Frost & Sullivan’s Industrial Automation & Process Control Team

The emerging economies of India, Brazil and China have made headlines for more than two decades now, on the back of rapid economic development coupled with reduction of poverty and rising spending power on an unprecedented scale. Meanwhile, from the developed economies’ point of view, after just having recovered from acute financial crises, the economies are finally on the way to returning to solid growth. However, when we look at it below the national level, the key powerhouses of growth for most of these economies, be it, developed or developing, are the growing number of mega cities in these regions. The rapid rate of industrialization and growth stemming from the world’s 750 biggest cities is resulting in a boom in the number of diverse and skilled labor forces and is collectively contributing towards the growth of global GDP. Currently, these mega cities account for nearly 57 percent of the global GDP and by the end of 2030, they are expected to add a staggering US$ 80 trillion to the global economy, making up almost 61% of the total.

Definition of Mega Cities:

A Mega City is defined as an urban area with a population of more than 8 million and a gross domestic product (GDP) of at least $250 billion. However, a Smart City is an enabling platform built by the government to manage interactions among people and the infrastructure in a city to guide policy-making through the intelligent use of technology. North America is the most urbanised region in the world, with 83.7 percent of the population living in urban areas in 2016. In contrast, the African population is one of the most rural, with only 40 percent living in urban areas in 2016, despite it being one of the fastest urbanizing regions. In Asia, however, the fastest growing urban agglomerations are medium-sized cities (with less than 1 million inhabitants) located in and by 2025, the urban population in Africa is expected to reach 56 percent of the total.

Future of Infrastructure—Emergence of Smart Cities in Africa:

With growing promise of mega regions in Africa, the region is bound to become the next frontier of growth and opportunity for multi-national companies, globally, by the end of 2025. By 2025, it has been estimated that nearly 50 percent of the total continent’s population will reside in cities. These cities will be home to over 4 billion consumers and about 2 billion of these consumers will be part of emerging market cities. The emergence of megacities are expected to be a source for the development of at least six other cities including Johannesburg, Luanda, Nairobi, Addis Ababa, Casablanca, and Khartoum by 2025–2030.

With growing promise of mega regions in Africa, the region is bound to become the next frontier of growth and opportunity for multi-national companies, globally, by the end of 2025. By 2025, it has been estimated that nearly 50 percent of the total continent’s population will reside in cities. These cities will be home to over 4 billion consumers and about 2 billion of these consumers will be part of emerging market cities. The emergence of megacities are expected to be a source for the development of at least six other cities including Johannesburg, Luanda, Nairobi, Addis Ababa, Casablanca, and Khartoum by 2025–2030.

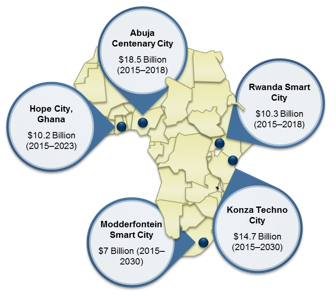

One of the primary focuses of South Africa’s Modderfontein Smart City is to develop its infrastructure, and in the next 15–20 years, the city will have about 30,000 to 50,000 housing units that can accommodate over 100,000 residents. The project is currently valued at $7 billion for 2015–2030, and is expected to become a financial hub for the whole of Africa by the end of 2030. The project can potentially result in doubling the requirement of cement and water than the current levels, to develop this smart city.

Nigeria’s Abuja Centenary City will be a smart, inter-connected urban center, and will potentially become a business magnet on the African continent by the time the city is developed. The city is designed to accommodate several top-end business and technology parks, residential districts and industry financial centers. Currently, the project is valued at $18.5 billion for the period 2015–2018, while the entire project is expected to touch $180.6 billion with a completion period of 2025. The city also plans to have a sound water management system in place where the approximately 60 percent of the water will be recycled and the wastewater is used as many times as possible.

Impact on the Pumps Industry:

The year 2014 saw 46.2 percent growth in investment by value of mega projects under construction in Africa, in addition to a $100.4 billion investment in 2014 ($222.4 billion in 2013). Abuja Centenary City is the second-largest smart city project globally, where 16 private sector companies are going to invest $4 billion in developing 10 districts of the city.

The emergence of these Mega Smart Cities is pushing up demand for use of pumps in the construction sector and is opening huge growth opportunities for centrifugal pumps in the region. Ironically, though, use of submersible pumps in the African construction sector is witnessing a higher rate of repairs and maintenance rather than replacements which is, in turn, resulting in a slower growth of submersible pumps in the sector. On the contrary, growth of other pump types such as lobe and axial & mixed flow are expected to be about 2.5–4 percent in FY 2017.

Smart Cities—Future Outlook of Asia-Pacific:

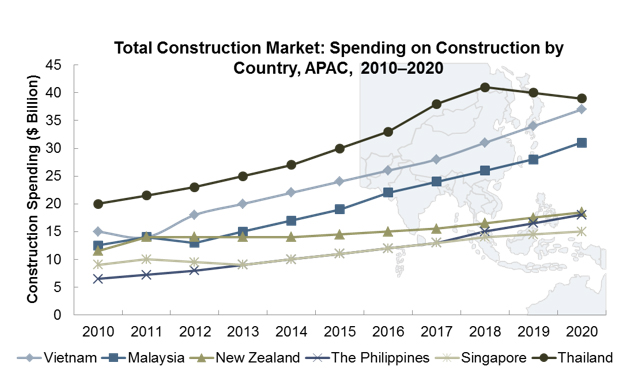

Massive economic development pans in APAC is giving rise to several disruptive and dynamic business models such as smart cities and infrastructure enhancement in the region which is that is aimed at building environmentally-responsible and resource-efficient Mega Cities. It has been estimated that, despite the market being in early recovery stage, most countries in APAC are bound to exceed the US in the construction sector, driven by India and China. This will increase mega sustainable and energy-efficient structures that not only bring down total energy cost, but also decrease the urban heat island effect which is a major concern in Southeast Asian countries.

Governments of APAC countries are currently offering fiscal/ financial incentives, grants, and subsidies to households and industry facilities to encourage home owners and building contractors to invest in energy-efficient buildings. For example, the Grant for Energy Efficient Technologies (GREET) in Singapore and the Local Government Energy Efficiency Program (LGEEP) in Australia.

The acceleration of the urbanization process in China has boosted demand in terms of water, gas, heat and other municipal infrastructure supplies. To keep pace with future demand, the government has decided to invest $1,120 billion in municipal infrastructure construction throughout the 12th Five-Year Plan.

Considering the government target of 36 million units of indemnificatory apartment projects and more than 60 megaprojects of infrastructure construction during the 12th Five-Year Plan, as well as a $480 billion investment in rural area infrastructure (2011-2020), the production of construction chemicals is anticipated to experience continuous growth. Strong demand from public infrastructure projects in China, and India too to an extent, presents growth opportunities for pump companies focused on chemicals industry.

Impact on the Pumps Industry:

In APAC, centrifugal pumps dominate the construction chemicals industry and makes up almost 77 percent of the total revenues. The pumps industry in construction is expected to grow by 1.2 percent in 2016 and is expected to display a CAGR of 2.2 percent for the time-period 2017-2019. APAC, being a price-conscious market, companies tend to aggressively price their existing products instead of foraying into value-added sustainable solutions. Hence, pump companies will need to focus on boosting aftermarket sales revenue to compensate for the loss in new project sales.

Mega Cities—Overview in North America:

The United States is one of the world’s most important markets for construction, which experienced a lot of turbulence during the 2008 recession and economic crisis. However, activities in the commercial and residential construction sectors are improving and slowly going down the recovery path, driven solely by rising consumer spending and improving employment rate in the country. In the US, some of the biggest investments are being made in the state of New York, coming from major contractors from China and Europe.

While in the US, CAPEX investment in commercial buildings is expected to reach $235.64 billion by the end of 2017, in Canada, projected growth in CAPEX is expected to continue to be slow in 2017, owing to decline in investments in the non-residential sector, as a result of slowdown in oil and gas, power generation, and government engineering structures.

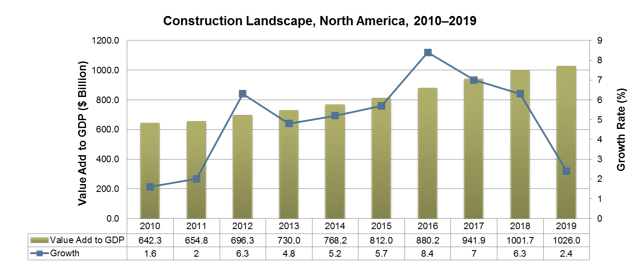

The GDP from the construction sector rose to $812.00 billion in 2015—up from a low of $642.28 billion in 2010—displaying a growth of 4 percent for the time period in between.

Construction activities have been forecast to display a healthy growth from 2016 to 2018, before which it might dip a bit. Overall, the contribution of construction toward US’s GDP is expected to touch $880.22 billion by the end of 2016 and $1,026.01 billion by 2019, by when the growth rate is expected to decline markedly.

Impact on the Pumps Industry:

The North American commercial pumps market witnessed a growth of 3.0 percent in FY 2016 chiefly due to rising investments in infrastructural development and major building construction projects in the region. One of the biggest trends that the Canadian construction sector is witnessing is the shift in focus toward green buildings that are energy and water-efficient and address air quality and material resource conservation.

Of the different pump types used in the commercial sector, single-stage pumps are the dominant technology, accounting for almost 34.4 percent of the pumps market of North America. Single-stage pumps are predominantly used in HVAC and pressure boosting applications in the region and are expected to generate revenues worth $229.4 million in 2016. It has been forecast to grow at a CAGR of 4.0 percent between 2015 and 2021.

The share of PD pumps in the North American commercial sector is comparatively less and accounts for 6.2 percent of the total pumps market. They are used in niche markets, such as condensate and dosing applications. The PD pumps market is expected to generate revenues of $51.6 million in 2021 and is forecast to grow at a CAGR of 4.6 percent between 2016 and 2021.

The Last Word

Mega Smart cities will thrive with dynamic business models in a disruptive environment; technology and governance will be key enablers for participants in this ecosystem. This trend will act one of the biggest drivers of growth for the pumps industry worldwide.

Growing demand for energy-efficient pumps, reinstated by newly implemented government mandates and regulations, will result in more and more companies developing advanced design pumps with more electronic features that would enable better system integration and system efficiency. Rising focus on energy efficiency and cost savings by way of efficient use of water in buildings will most likely increase between 2016 and 2021. This period will see the highest demand for pumps that comply with government directives for energy-related equipment.

About Frost & Sullivan

Frost & Sullivan, the Growth Partnership Company, works in collaboration with clients to leverage visionary innovation that addresses the global challenges and related growth opportunities that will make or break today’s market participants. For more than 50 years, we have been developing growth strategies for the global 1000, emerging businesses, the public sector and the investment community. Register with us to start a discussion about what most interest you!

Comments