The U.S. water sector is entering a period of rapid change. Long seen as a slow-moving, predictable and steady component of critical infrastructure, water now faces mounting external pressures—from construction slowdowns to AI-driven demand spikes. For utilities, industrial users, and investors, this disruption brings both risk and opportunity – reshaping how water is financed, managed, and sourced.

As part of our ongoing, in-depth analysis of the global water sector, Bluefield Research’s team of water experts has identified five key dynamics that are changing water management in the U.S. Together, they form the contours of a sector that is no longer business as usual.

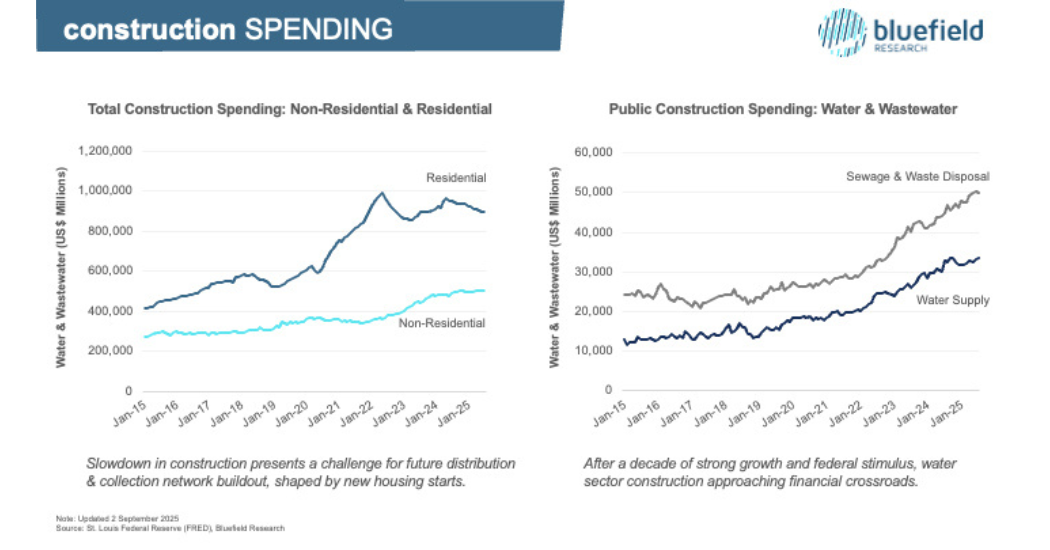

1. Construction Slowdown: Asset Renewal Over Expansion

The longstanding link between housing growth and water infrastructure expansion is weakening. Residential construction has dropped 15% since its 2022 peak, disrupting the historical model in which new homes meant new pipes, treatment capacity, and customer connections. For decades, utilities could rely on consistent construction activity to justify system expansion—but that era is ending.

In its place, a new paradigm is emerging: one that prioritizes upgrading and renewing existing assets over building new ones. Capital investment is increasingly flowing toward resilience projects—digital twins, leak detection, smart meters—that optimize aging infrastructure. As climate uncertainty grows and water supply becomes more variable, this shift from expansion to efficiency will only accelerate.

Public spending on sewage and waste has doubled to US$50 billion over the last decade. Although, declines in residential construction (-15% from its 2022 peak) threaten greenfield infrastructure capacity additions.

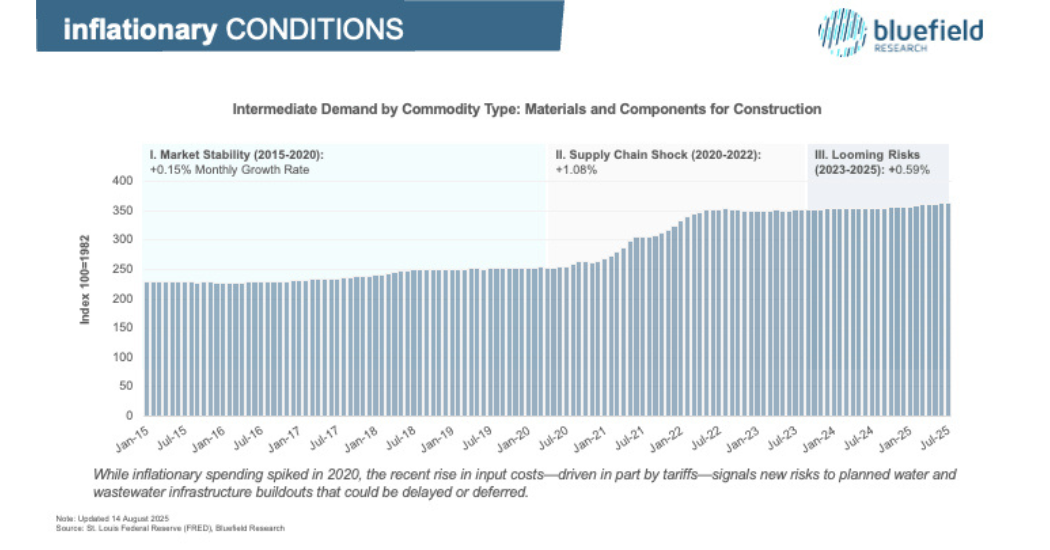

2. Inflation and Tariffs: The New Cost Reality

Cost predictability—once a defining feature of water infrastructure planning—is rapidly becoming a thing of the past. For nearly two decades before 2020, utilities and industrial users could rely on stable material prices to guide long-term budgets. That era of stability has unraveled. First came pandemic-era supply chain disruptions, followed by sharp swings in commodity prices, and now renewed tariffs on critical imports like steel and chemicals.

- 2015–2020: Construction material prices increased just 0.15% per month, supporting low-risk, long-range planning.

- 2020–2022: Price hikes surged to 1.08% per month, forcing utilities to revise project budgets in real time.

- 2025 Outlook: New tariffs are compounding cost pressures, with project deferrals likely in 2026 due to delayed budget cycle impacts.

- Result: Bluefield’s analysis of capital improvement plans shows a 52% jump in per capita water utility spending (2023–2025)—a clear sign of inflation’s growing footprint.

What was once a cyclical nuisance is now a structural challenge. In this new cost environment, the winners will be utilities and contractors that adapt—rethinking procurement strategies, strengthening supply chains, and embedding technology to mitigate financial risk.

Rising construction material costs—ticking upward since the start of 2025—signal broader tariff impacts that could slow water and wastewater infrastructure buildout in 2026.

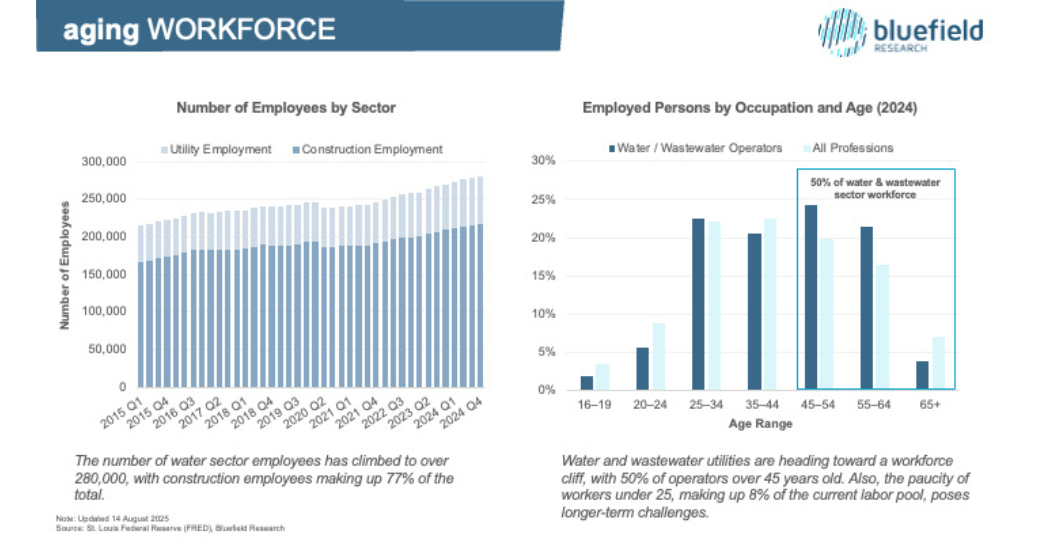

3. Workforce Cliff: Aging Operators, Thin Pipeline

The once-stable water workforce is entering a period of accelerated attrition. What was a quietly aging labor force is now approaching a tipping point. According to the Bureau of Labor Statistics, nearly half of all U.S. water and wastewater operators are over 45 years old, while only 8% are under 25—a clear warning sign of a thinning talent pipeline. As retirements rise and turnover accelerates, utilities can no longer rely on institutional knowledge and long-serving staff to maintain operations.

This shift demands a new workforce strategy. Training, recruitment, and succession planning must move to the top of the agenda, supported by a coordinated push to attract younger talent. At the same time, utilities are increasingly turning to automation, remote monitoring, and AI-driven analytics to ease labor pressures and ensure continuity. Expanded apprenticeship programs, partnerships with community colleges, and the adoption of technologies that reduce dependence on on-site staffing all point to a broader industry pivot—from labor-intensive operations to tech-enabled resilience.

Water and wastewater utilities are heading toward a workforce cliff, with 50% of operators over 45 years old. The paucity of workers under 25, making up 8% of the current labor pool, poses longer-term challenges.

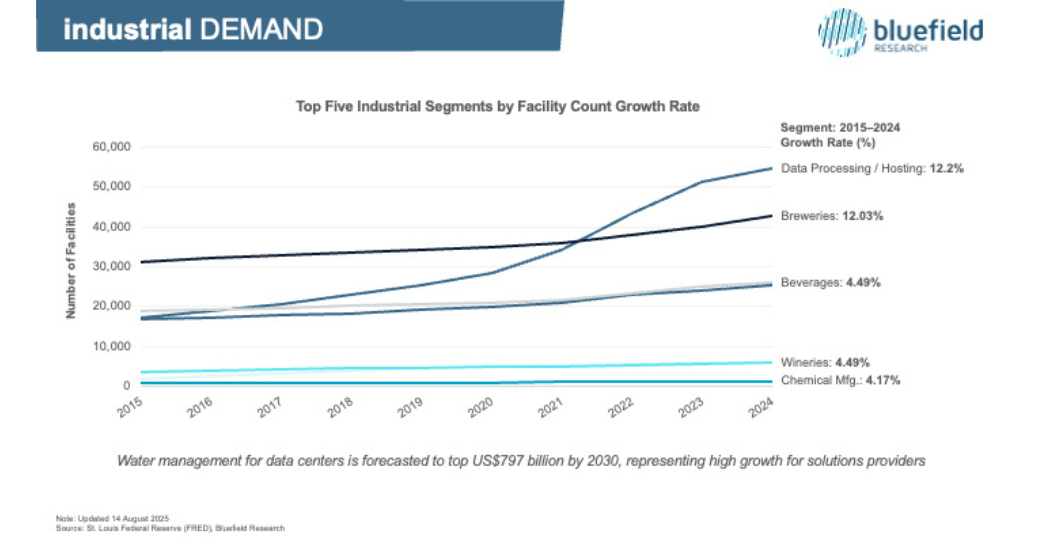

4. Industrial Surge: Data Centers Drive Demand

Industrial water demand is undergoing a dramatic shift—from steady, sector-based consumption to surging, infrastructure-intensive growth driven by digital infrastructure. What was once a niche consideration—data centers—is now one of the most powerful forces reshaping the U.S. industrial water landscape. Since 2015, the number of data center facilities have increased by 12.2% annually, outpacing conventional water-intensive sectors such as chemicals, paper, and food & beverage.

The U.S. industrial water market is currently valued at US$388 billion, with water management related to data centers expected to more than double—reaching US$797 billion globally by 2030. This shift is creating intense pressure on local water resources while simultaneously presenting major opportunities for innovation in cooling, reuse, and efficiency technologies.

At the same time, reputational and regulatory scrutiny is rising. Data center operators are responding with investments in watershed restoration, community partnerships, and transparent water reporting. What began as a quiet corner of industrial demand is now at the center of a broader transformation—pushing industrial water management toward a future defined by efficiency, resilience, and environmental accountability.

Growing at 12.2% annually since 2015, the data center segment is amplifying pressures on water resources and energy systems within a US$388 billion industrial water sector.

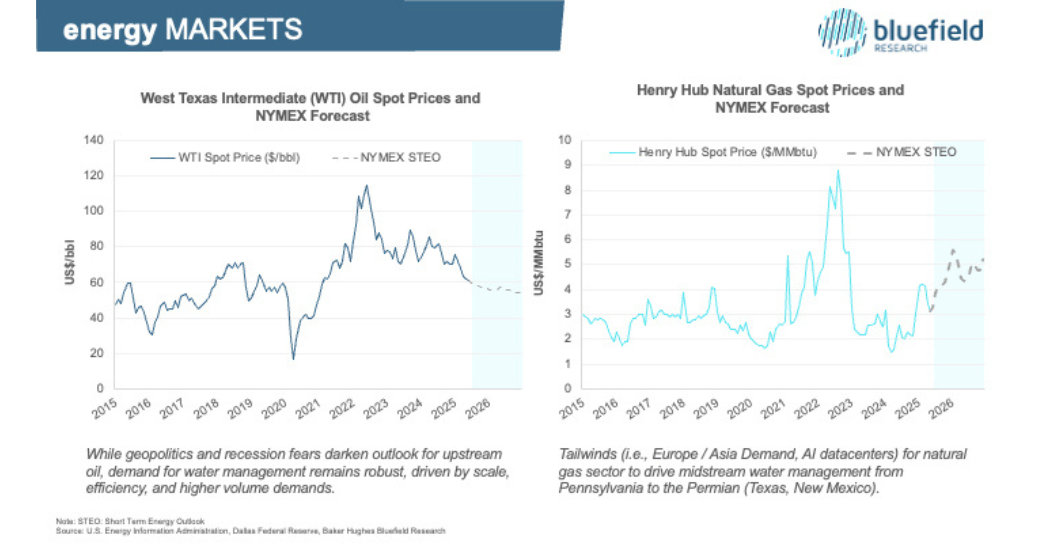

5. Energy-Water Nexus: Midstream Water Goes Mainstream

The role of water in energy production is no longer just cyclical—it’s becoming structural. Once viewed as a niche and highly price-sensitive service within oil and gas operations, midstream water services have evolved into a US$28 billion industry, encompassing supply, treatment, transport, and disposal in upstream operations. The foundation of demand has changed: the sector is now reinforced by enduring, global structural influences—Europe’s pivot away from Russian gas, Asia’s growing appetite for LNG, and a surge in U.S. electricity demand from AI and data centers.

This marks a significant shift. Water is no longer a reactive input that flexes with commodity swings; it has become a critical enabler of energy continuity and growth. In parallel, the industry is transitioning from high-disposal models to a reuse- and efficiency-driven future. A growing number of midstream water companies are consolidating and scaling technologies focused on produced water recycling, reducing environmental impact while improving operational efficiency. Together, these dynamics signal a maturing and increasingly indispensable role for water in the energy value chain—where sustainability, scalability, and resilience are becoming competitive advantages.

Water has always been essential. Now, it’s dynamic, disruptive, and increasingly strategic. The next decade will reward those who adapt—whether through technology, partnerships, or bold investments. The question isn’t if the water sector will change—but who will lead that change.

Midstream water management has emerged as a US$28 billion service industry, delivering critical water services—supply, storage, treatment, transport, and disposal–across seven key basins.

Originally publish at Bluefield Research