The U.S. municipal water sector, which has traditionally been slow to adopt new technologies, sits at the cusp of change with over $20 billion of forecasted spending on software, data, and analytics solutions over the next decade. As a result, more than 40 companies are positioning to deploy state-of-the-art solutions to enable more advanced levels of system intelligence, real-time network visibility, energy efficiency, and customer management, according to a new report from Bluefield Research, US Smart Water: Defining the Opportunity, Competitive Landscape, and Market Outlook.

A number of factors, including state legislation for water loss, aging infrastructure, and pressure on utilities to be more efficient, are driving interest in what is more commonly known as smart water. “Historically, utilities have been hobbled by their inability to generate actionable insights from disparate network and water usage data, but this is changing with more advanced data management and cloud-based solutions,” says Will Maize, a Senior Analyst at Bluefield Research. “Early adopting utilities, including American Water and East Bay Municipal Water District, are leading the shift towards smart water technology adoption.”

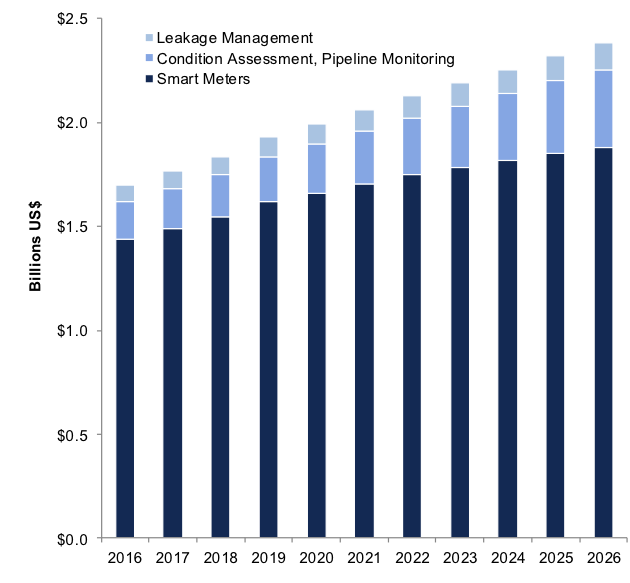

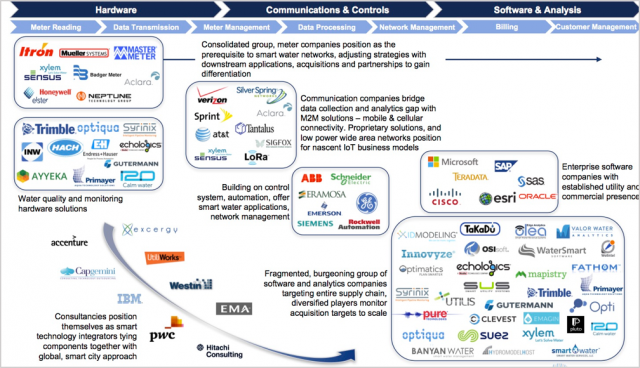

In the near-term, advanced water meters (e.g. AMR, AMI) will represent the lion´s share of forecasted expenditures at 82% from 2017 through 2026. A consolidated group of established metering players are expanding their product and service portfolios to leverage the value of data collected through their installed hardware. Market leaders, including Mueller and Itron, have moved downstream into communications, data management and analytics, while recent market entries via acquisition by Xylem and Honeywell will further reshape the competitive landscape.

At the same time, over US$2.7 billion will be directed towards asset condition assessment and pipeline monitoring through 2026. Operating expenditures on leakage management will total $1 billion through the forecast period, according to Bluefield Research.

While smart meters garnered the most attention, asset intelligence and visibility into real-time network conditions offer significant benefits,” says Mr. Maize. “Water companies can now go from being reactive to proactive.”

Seizing on this burgeoning demand for solutions is an outside group of venture-backed start-ups seeking to leverage their data expertise, much of which draws from other industry applications. These data and analytics companies are looking to integrate disparate sources of data to optimize networks, track water quality, and generate insights for asset performance management. Their primary challenge, however, will be overcoming a credibility gap with demonstrated pilot projects and buy-in from municipal utilities. A select group of companies from more mature smart water markets, Europe and Israel, are also beginning to make headway in the U.S. market.

Exhibit: US Smart Water Value Chain

Making inroads into 50,000 U.S. municipal water systems is no small task for vendors, particularly the new entrants without proven track records. The challenge is further heightened by their need to navigate utilities’ operating silos- back office operations, billing and revenues, and network operations.

The market is already beginning to take on a different shape. We are seeing larger, diversified companies enter the fray, utilities reshaping their mindset, and Silicon Valley-types applying data expertise. This combination has huge potential to change the way the U.S. water industry works,” says Mr. Maize. “If you looked at the smart water market a few years ago, there were just a handful players.”

About Bluefield Research

Bluefield Research provides data, analysis and insights on global water markets. Executives rely on our water experts to validate their assumptions, address critical questions, and strengthen strategic planning processes. Bluefield helps key decision-makers at municipal utilities, engineering, procurement, & construction firms, technology and equipment suppliers, and investment firms advance their water strategies. Learn more at www.bluefieldresearch.com.